Keywords

Reports

Investment Decision

ESG

How to Cite

Abstract

Purpose: To conduct an experimental study with Brazilian investors to investigate the impact of ESG information on investment decisions, notably information regarding worker safety measures taken by publicly traded companies to mitigate the effects of the COVID-19 pandemic during an economic crisis caused by COVID-19

Methodology/approach: The experiment involved 70 participants, divided between specialists and non-specialists in the business field, who responded to questions about fund allocation preferences when exposed to conventional and ESG information sets. T-tests and one-way ANOVA were used to test the hypotheses.

Originality/Relevance: The justification for this study lies in the need to test the findings of Belkaoui (1980) and contemporary literature on the impact of ESG disclosure in the context of a profound health, social, and economic crisis caused by the pandemic.

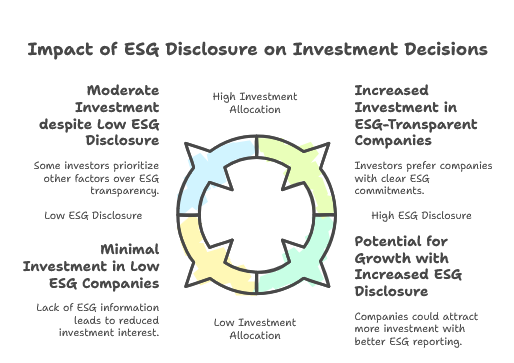

Key findings: In this study, it can be concluded that companies receive larger investment amounts when they disclose ESG information regarding the company’s actions in sustainability, governance, inequality reduction, and measures to address the COVID-19 pandemic, and that in the presence of ESG information, investors allocate their funds to companies with better performance in these indicators."

Theoretical/methodological contributions: The study expands the existing literature on the impact of ESG information on investment decisions. Methodologically, the hypotheses of the linguistic relativity paradigm in accounting were validated through an experiment with Brazilian investors, involving both specialists and non-specialists, allowing for a more robust analysis of perceptions regarding ESG information.

References

Adams, C. A. & Frost, G. R. (2008) Integrating sustainability reporting into management practices. Accounting Forum. 32(4), 288-302.

Avelar, E.A, Ferreira, P,O. & Fereira, C.O. (2020) Covid-19: Análise dos Efeitos e das Medidas Adotadas pelas Companhias Abertas Brasileiras Frente à Pandemia. Anais XX USP Conference in Accounting. São Paulo- SP.

Ball, R.J. & Brown, P. (1968), An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6 (2),159-178.

Beaver, W.H. (1968). The information content of annual earnings announcements. empirical research in accounting: selected studies 1968. Journal of Accounting Research. 6 (Supplement), 67-92.

Belkaoui, A.R. (1980). The impact of socio-economic accounting statements on the investment decision: an empirical study. Accounting, Organizations and Society. 5(3). 263- 283.

Banco Central do Brasil. (2020). Focus: Relatório de Mercado: Expectativas de Mercado.

Fonte: https://www.bcb.gov.br/content/focus/focus/R20200515.pdf

Casella, G. & Berger, R.L. (2002) Statistical Inference.Duxbury. 2ª ed.

Chan, C.& Milne, M. (1999). Investor reactions to corporate environmental saints and sinners: an experimental analysis. Accounting and Business Research, 29 (4), 265-279.

Cheng, M.M., Green, W.T. & Chi Wa Ko, J. (2015). The impact of strategic relevance and assurance of sustainability indicators on investors’ decisions. Auditing: A Journal of Practice & Theory, 34 (1), 131-162.

Deegan, C. & Rankin, M. (1997). The materiality of environmental information to users of annual reports. Accounting, Auditing and Accountability Journal.10 (4), 562-583.

De Zwaan, L., Brimble, M. & Stewart, J. (2015). Member perceptions of ESG investing through superannuation. Sustainability Accounting, Management and Policy Journal.6(1). 79- 102.

Eccles, R.G., Serafeim, G. & Krzus, M.P. (2011). Market interest in nonfinancial information”, Journal of Applied Corporate Finance. 23(4), 113-128.

Guidry, R.P. & Patten, D.M. (2010). Market reactions to the first-time issuance of corporate sustainability reports: evidence that quality matters, Sustainability Accounting, Management and Policy Journal.1(1). 33-50.

Holm, C. & Rikhardsson, P. (2008). Experienced and novice investors: does environmental information influence investment allocation decisions? European Accounting Review, 17(3). 537-557.

Johns Hopkins University. (2020). Coronavirus Resource Center. Fonte: Covid-19 Map: https://coronavirus.jhu.edu/map.html

Khemir, S., Baccouche, C. & Ayadi, S.D. (2019). The influence of ESG information on investment allocation decisions: An experimental study in an emerging country. Journal of Applied Accounting Research. 20 (4). 458-480.

KPMG (2015). Currents of change. The KPMG International Survey of Corporate Responsibility Reporting. www.kpmg.com.

Lorraine, N.H.J., Collison, D.J. & Power, D.M. (2004). An analysis of the stock market impact of environmental performance information. Accounting Forum, 28 (1), 7-26.

Milne, M. & Chan, C. (1999). Narrative social disclosures: how much of a difference do they make to investor decision-making? British Accounting Review. 31 (4), 439-457.

Rikhardsson, P. & Holm, C. (2008). The effect of environmental information in investment allocation decisions-an experimental study. Business Strategy and the Environment. 17 (6). 382-397.

Teoh, H.Y. & Shiu, G.Y. (1990). Attitudes towards corporate social responsibility and perceived importance of social responsibility information characteristics in a decision context. Journal of Business Ethics. 9 (1), 71-77.

Thompson, P. & Cowton, C.J. (2004). Bringing the environment into bank lending: implications for environmental reporting. The British Accounting Review. 36(2). 197-218.

Van der Laan Smith, J., Adhikari, A., Tondkar, R.H. & Andrews, R.L. (2010). The impact of corporate social disclosure on investment behaviour: a cross-national study. Journal of Accounting and Public Policy. 29 (2), 177-192.

Van Duuren, E., Plantinga, A. & Scholtens, B. (2016). ESG integration and the investment management process: fundamental investing reinvented. Journal of Business Ethics, 138 (3), 525-533.

Whitehouse, L. (2006). Corporate social responsibility: views from the frontline. Journal of Business Ethics.63(3). 279-296.

Xu, X.D., Zeng, S.X. & Tam, C.M. (2012). Stock market’s reaction to disclosure of environmental violations: evidence from China. Journal of Business Ethics.107(2). 227-2

This work is licensed under a Creative Commons Attribution 4.0 International License.

Copyright (c) 2024 Journal of Sustainable Competitive Intelligence